Abu Dhabi Islamic fintech sits at the intersection of regulation, digital infrastructure, and demand for Shariah-compliant products. Abu Dhabi Global Market (ADGM) and NYU Abu Dhabi data placed the emirate first globally for regulatory innovation in the inaugural Financial Centre Competitiveness Index (FCCI). Abu Dhabi ranked 12th globally overall in that index. That regulatory positioning was operationalised through the launch of the FinTech, Insurance, Digital and Alternative Assets (FIDA) cluster, designed to consolidate the emirate’s fintech landscape and build an integrated global financial ecosystem that harnesses capital, innovation, advanced technologies, and AI solutions.

The FIDA cluster comes with clear economic targets that matter for founders and financial institutions building Shariah-compliant digital finance. Abu Dhabi officials forecast the cluster will add AED56bn to Abu Dhabi’s GDP by 2045. The same initiative is forecast to generate 8,000 skilled new jobs and attract at least AED17bn. These targets matter because Islamic fintech often needs specialist talent across product, compliance, cybersecurity, and engineering. The cluster’s unified approach also supports firms that want to combine regulated finance with digital assets and AI-driven capabilities.

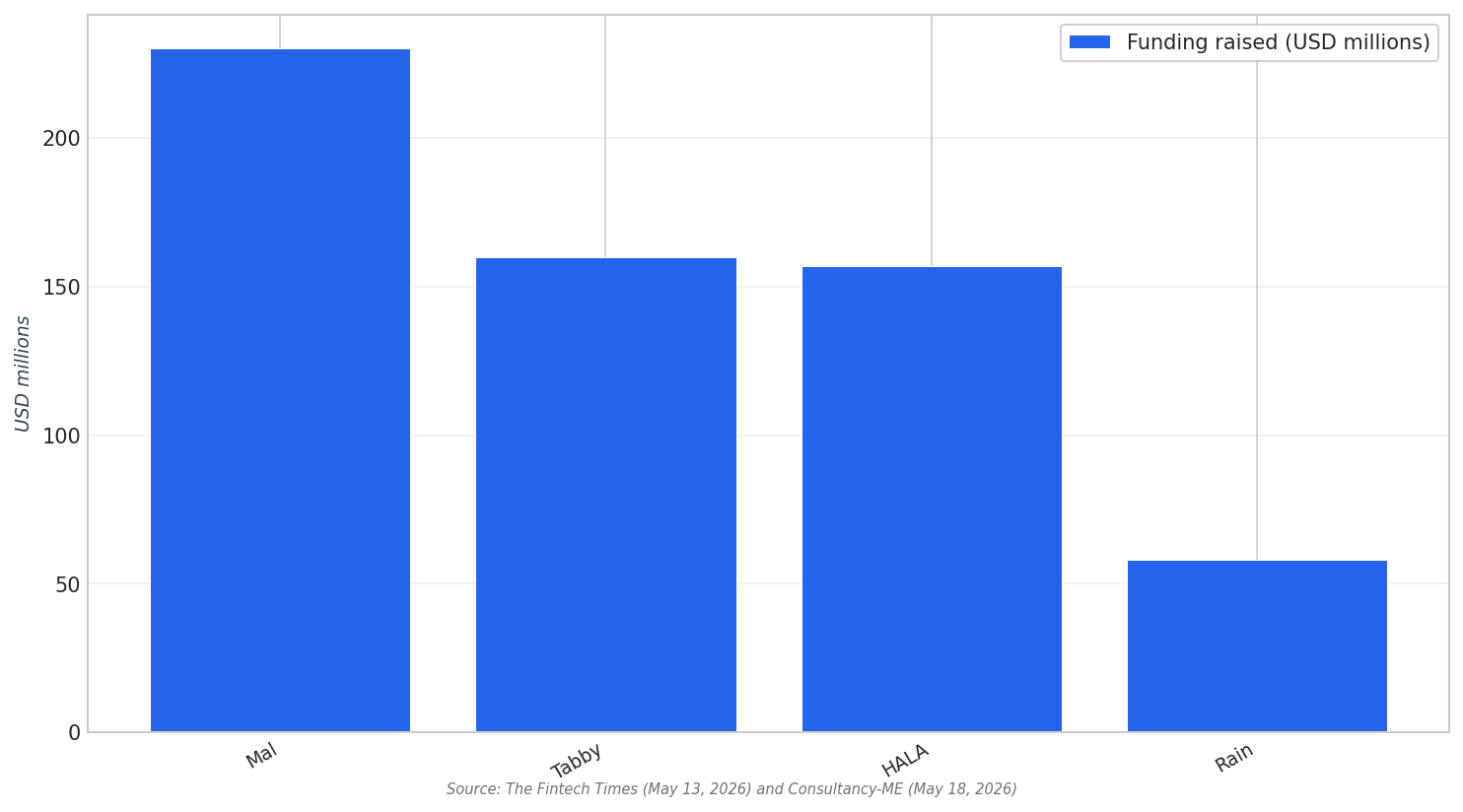

Regional fintech momentum supports Abu Dhabi’s opportunity set, even in a cautious global funding environment. In 2025, venture capital funding across MENA reached $3.8 billion. High-profile transactions included Rain raising $58 million, HALA raising $157 million, and Tabby securing $160 million. Another major raise cited in the same funding cycle was AI-native Islamic bank Mal at $230 million. For Abu Dhabi Islamic fintech builders, this funding picture signals investor conviction in infrastructure plays and digital-first financial models that can scale across the region.

Where Shariah-Compliant Digital Finance Can Scale Fast

Multiple sources highlight structural opportunity areas poised for immediate disruption that map directly to Islamic fintech product design. These include SME financing for underserved enterprises, cross-border payments that reduce cost and increase speed using digital rails, and digital wallets as a leapfrog technology for financial inclusion. They also highlight digital-first Islamic finance products as under-developed relative to demand, with opportunities across savings, lending, and wealth management. For product teams, this creates a practical playbook: start with clear customer pain, then deliver Shariah-compliant user journeys with digital distribution and fast onboarding.

Technology priorities in the region also point to how Abu Dhabi Islamic fintech can execute. Survey respondents ranked embedded finance highest at 34 per cent, followed by artificial intelligence and machine learning at 29 per cent, and open banking at 21 per cent. That mix supports partnerships where Islamic finance features can be delivered inside non-bank customer experiences, while AI helps with operational automation and risk workflows. At the same time, trust remains a gating factor. Abu Dhabi Islamic Bank (ADIB) explicitly framed cybersecurity as fundamental to trust in digital banking and financial services, and said engaging startups can identify practical, scalable solutions that strengthen resilience.

What does “Abu Dhabi Islamic fintech” focus on in practice?

Why does regulation matter for fintech growth in Abu Dhabi?

What funding signals support regional fintech momentum relevant to Abu Dhabi?

Which technologies are most associated with near-term fintech opportunity?